INTRODUCTION

A Non–Banking Financial Company (“NBFC’s”) is known as a company, which is indulged in providing financial services similar to banks such as, loans and advances, acquisitions of shares, debentures, stocks and other marketable securities without the need of possessing a banking license.

In India, Reserve Bank of India (“RBI”) acts as one of the crucial regulatory body governing financial sector in India. Therefore, any company incorporated and formed under Companies Act, 2013 or 1956 intending to provide aforementioned financial services is required to be registered as an NBFC under Section 45-I of the Reserve Bank of India Act, 1934 (“RBI Act).

Therefore, in view of the above the FinTech companies, which uses technology to automate and enhance procedure of providing financial services in an efficient and faster manner, is also required to be registered as a NBFC.

In recent years, the FinTech companies as a result of profound customer demand, Digital India initiative, higher tech awareness, growing investment platforms, favorable demographics, and enabling Government policies has witnessed exponential growth in India over the past few years and is now amongst the fastest FinTech growing markets in the world.

The RBI considering the rapid growth of the FinTech market in India, higher risk appetite of NBFCs, which has enabled them to contribute to their size, complexity, interconnectedness with the financial system and making some of the entities systemically significant, posing potential threat to financial stability, has led to the introduction of Scale Based Regulation for NBFC’s, which will come into effect on 01.10.2022 to provide a more robust and organized regulatory framework for NBFC’s.

In this article we will attempt to discuss about what SCALE Based Regulation is and its regulatory framework and the evolution matrix stating, why such regulatory change was required.

THE SCALE BASED CLASSIFICATION

The RBI vide Notification No. RBI/2021-22/112 dated 22.10.2021 has issued the regulations and directions pertaining to the framework of Scale Based Regulations (SBR) that encompasses various aspects of the NBFC’s with respect to capital requirements, governance standards, prudential regulation, etc.

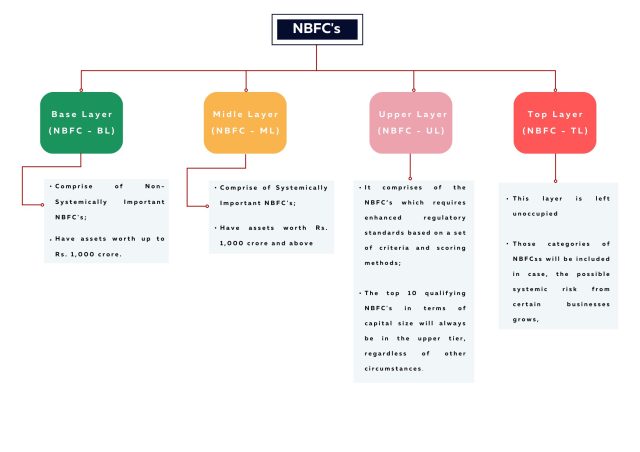

As per the SBR, the regulatory structure of the NBFCs shall be comprising of Four Layers based on their size, risk and activities.

1. Base Layer (NBFC-BL) – This layer comprises of non-systemically important NBFCs, which requires the least regulatory intervention and have assets worth up to Rs. 1,000 crore.

This is where the majority of NBFCs will fall. This layer comprises of

i. NBFC-Peer to Peer Lending Platform (NBFC-P2P),

ii. NBFC-Account Aggregator (NBFC-AA),

iii. Non-Operative Financial Holding Company (NOFHC)

iv. NBFCs not availing public funds and not having any customer interface

2. Middle Layer (NBFC-ML) – This category is comprises of systemically important NBFCs with assets of Rs 1,000 crore or more such as, deposit taking NBFCs (NBFC-D), NBFC Infrastructure Debt Fund (NBFC – IDFs), standalone primary dealers, NBFC Core Investment Companies (NBFC – ICC), NBFC Home Finance Companies (NBFC – HFs), and NBFC Infrastructure Financing Companies (NBFC – IFCs).

3. Upper Layer (NBFC-UL) – This category comprise of the NBFC’s which requires enhanced regulatory standards based on a set of criteria and scoring The top 10 qualifying NBFCs in terms of capital size will always be in the upper tier, regardless of other circumstances.

4. Top Layer – This layer is left unoccupied and those categories of NBFC’s will be included in case, the possible systemic risk from certain businesses grows, NBFCs falling within the upper layer may be transferred to the top layer, as per the RBI’s assessment.

The Regulatory Framework

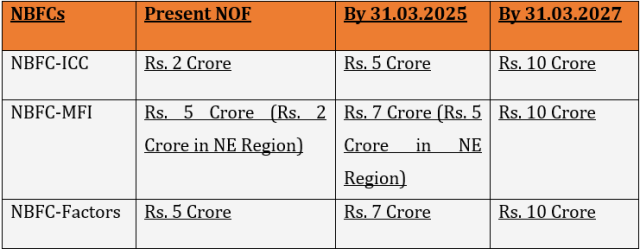

1. Net Owned Fund – The regulatory minimum net owned fund (NOF) for NBFC microfinance institutions (NBFC-MFI), NBFC investment and credit companies (NBFC-ICC), and NBFC-Factors is required to be increase to 10 crore in the next 7 years.

However, the NBFC’s categorized in the Base layer i.e., NBFC-P2P, NBFC-AA, and NBFCs with no public funds and no customer interface, shall continue to be RS. 2 crore.

2. Credit Concentration Restrictions – The NBFC’s indulged in lending and investing have been combined and provided a single exposure limit i.e., of 25% of Tier 1 capital for an Individual borrower/party & 40% of Tier 1 capital for a single group of borrowers/parties.

3. NPA Classification – Then RBI has altered the criteria regarding categorizing loans as Non-Performing Assets (NPAs) and for all types of NBFCs, overdue payments of more than ninety days will henceforth be referred to as NPAs.

4. Experience of Board – Since, handling the affairs of a NBFC demands professional competence. Therefore, at least 1 of the directors must have relevant experience working in a bank or NBFC.

5. Embargo on IPO Funding – The RBI has also set a limit of Rupees 1 crore per borrower with respect to the funding of Initial Public Offer (“IPO”) subscriptions. However, NBFC’s are allowed to set more cautious and conservative limits.

6. Risk Management Committee – the RBI considering the higher risk appetite vide this regulation have asked the NBFC’s to create a Risk Management Committee (“RMC”), either at Board or Executive level, in order to better assess prospective and numerous risks, including liquidity risk, that might be faced by the NBFC’s in the rapid changing and evolving financial sector. The RMC shall submit its report to the NBFC’s Board of Directors.

7. Disclosures –The NBFC’s under the revised regulation, in view of better transparency is required to expand its horizon of disclosure and disclose all kinds of exposure, related party transactions, loans to Directors/ Senior Officers, income and expenditure of exceptional nature, Breaches in terms of covenants in respect of loans availed by the NBFC or debt securities issued by the NBFC including incidence/s of default and customer complaints etc.

8. Whistle-Blower Mechanisms – NBFC’s must implement Whistle-blower mechanism at the upper and middle layers, allowing whistle-blowers to disclose real concerns and mismanagement inside the organization.

9. Loan to Director, Senior Officers and Related Party –As per this regulation, NBF’s at the Base Layer (NBFC – BL) is required to maintain a board approved policy with respect to the grant of loans to directors, senior officers and relatives of directors and to entities where directors or their relatives have major shareholding.

10. Key Managerial Personnel – The Key Managerial Personnel (“KMP”), shall not hold any position including directorships, in any other i.e., NBFC-ML or NBFC-UL, except for directorship in a subsidiary company. A time period of two years is provided with effect from 01.10.2022 to ensure compliance with the same.

11. Independent Director –The Independent Directors of a NBFC shall not be the board member of more than three NBFC’s at the same time, be it of NBFC – ML or NBFC – UL, Further, the NBFC shall make sure that no conflict will arise, in case the Independent Director becomes board member of other NBFC at the same time. A time period of two years is provided with effect from 01.10.2022 to ensure compliance with the same

12. Chief Compliance Officer – The RBI considering the higher risk appetite and the impact of NBFC’s on the financial sector have asked the NBFC’s to appoint a Chief Compliance Officer to incorporate an efficient and effective compliance culture and a strong compliance risk management framework.

THE EVOLUTION MATRIX

The RBI acquired the power to regulate NBFC’s in the year 1964, since then the RBI’s power over NBFC’s have been enhanced with the change in time and the regulations governing NBFC’s has witnessed a huge turnaround.

The regulatory framework for NBFC’s was first introduced in the year 1998, wherein the NBFC’s were classified based on accepting and not accepting deposits i.e., Public Deposit Accepting NBFC, Non-Deposit Accepting Core Investment Companies NBFC and Non-Public Deposit Accepting NBFC.

However, considering the rapid growth in the Asset Size of the NBFC’s with the increase in demand of NBFC’s across the country, the need for change in regulatory framework arose and in the year 2006, the regulatory framework was amended and NBFC’s were classified based on its Asset Size i.e., NBFC’s with Asset Size of more than Rs. 100 crore were classified as Systematically Important NBFC-ND and NBFC’s below Rs. 100 crore Asset Size as Non- Systematically Important NBFC-ND.

The regulatory regime regulating the NBFC sector is built on the ‘principle of proportionality’ so that the required operational flexibility is accessible to such NBFC’s.

Therefore, with the rapid developments over the past few years, higher risk appetite of NBFCs, their growing size, complexities, interconnectedness with the financial system which is capable of transmitting shocks into the entire financial sector and making some of the entities systemically significant, posing potential threat to financial stability, have led to the introduction of Scale Based Regulatory structure for NBFC’s comprising of four layers based on their size, activity, and perceived riskiness.

Under this latest regulatory framework, the RBI has made a number of modifications in terms of corporate governance & compliance risk management, ensuring that NBFC regulatory requirements are nearly identical to those that apply to banks. These regulations are meant to guarantee that NBFC’s adhere to high governance & internal risk management requirements.

AMLEGALS REMARKS

The proposed framework intends to preserve financial stability by allowing smaller NBFC’s to have access to the adequate flexibility required for their growth through calibrated regulatory measures and incorporating robust and strong compliance risk management framework to keep a close eye on the NBFC’s at the top scale capable of causing disruption and shocks to the entire financial sector.

The RBI with the help of SBR has tightened the screws on numerous regulatory and compliance issues in terms of corporate governance & compliance risk management to ensure that NBFC’s are well managed and protected against different risks as a financial sector regulator and adhere to high governance & internal risk management requirements.

These regulatory changes brought in with the help of SBR Framework makes significant changes, which are likely to boost the NBFC sustainability in the future and help in exponential growth of the financial sector in India.

Team AMLEGALS assisted by Mr. Amitosh Dubey (Intern)

For any queries or feedback, feel free to get in touch with siddharth.kakka@amlegals.com or tanmay.banthia@amlegals.com.