INTRODUCTION

This new era of digitalization has an impact on various aspects of our lives including finance. In this new era, the mechanism of taking loans has been completely transformed from the traditional 3-6-5 formula to 3-1-0 formula.

Digital Lending Platform allows consumers to avail finance in an instantaneous, efficient, and secured manner and the success of these Digital Lending Platforms depend upon capturing of personal and professional data of the Borrower, and especially upon the use of credit information to evaluate credit history of its customers before disbursing the loan.

In India, credit information is governed as per the Credit Information Companies (Regulation) Act, 2005 (“the CIC Act”) and Credit Information Companies (Regulation) 2006 (“the CIC Regulation”) and the ecosystem under the CIC Act consists of –

- The Credit Information Companies – which governs and stores the credit information; and

- Credit Institutions or Specified Users – who can access such credit information in a regulated manner.

That as per Section 17 of the CIC Act, only specified users were authorized to access the credit information of the customer, and any sharing of credit information with entities other than Specified Users was considered unauthorized sharing. Therefore, since FinTech companies were not considered Specified Users, they were facing several issues in India.

However, the position has changed drastically with the introduction of an amendment in the CIC Regulations vide notification CG-DL-E-30112021-231472 dated 29.11.2021, wherein the Reserve Bank of India (“RBI”) has brought in these FinTech companies within the ambit of Specified Users, who are involved in the processing of information, for the support or benefit of credit institutions, provided these companies comply with the eligibility criteria issued vide press release dated 05.01.2022.

In this article, we will be discussing about the Credit Information Companies, the impact of RBI Notification allowing FinTech companies to access credit information, and, how it will help transform the FinTech sector in India.

THE CREDIT INFORMATION COMPANIES

The Credit Information Companies (“CIC”) in accordance with the CIC Act, collect financial information of the individuals or entities from the Credit Institutions such as banks and/or other financial institutions which are members of the CIC, and the same is analyzed and processed to prepare the Credit Report of these individuals or entities.

Thereafter, the Credit Report is provided to the Specified Users, which helps them determine the creditworthiness of individuals/entities applying for a loan or credit card.

There are four CICs in India, they are as follows:

1. The Credit Information Bureau Limited (CIBIL)

2. Equifax Credit Information Company

3. Experian Credit Information Company

4. High Mark Credit Information Services

In terms of Section 2(f) of the Act, Credit Institutions mean a banking company and includes:

1. Banks

2. An NBFC

3. A Public Financial Institution referred to in section 4A of the Companies Act, 1956

4. A Financial Corporation established by a State under section 3 of the State Financial Corporation Act, 1951

5. The Housing Finance Institution is referred to in clause (d) of section 2 of the National Housing Bank Act, 1987;

6. The companies engaged in the business of credit cards and other similar cards.

7. Any other institution, which the RBI may specify.

THE ECOSYSTEM

THE ROLE OF SUPERVISED USERS

A specified user, as stated above is an entity that collects sensitive credit information from the CIC and process it for reviewing and evaluating the risk of its customers, judge the creditworthiness of a borrower, and facilitate credit institutions in taking effective credit decisions. Provided, the Specified Users comply with the below-mentioned obligations:

- Ensuring accuracy of credit information in accordance with Section 19;

- Adopt principles for maintaining the privacy of credit information and protecting the information from unauthorized use in accordance with Sections 20 and 22.

THE IMPACT OF RBI NOTIFICATION ON FINTECH COMPANIES

That prior to the amendment brought in by RBI including FinTech companies within the ambit of Specified Users and allowing these FinTech companies to process Credit Information for the benefit of CIC.

The FinTech companies engaged in providing lending services or processing customer-related information were relying on Non-Banking Financial Companies (“NBFCs”) or the Financial Institutions as partners to process the credit information, as in accordance with the CIC Act only authorized users were able to access credit information.

Therefore, the RBI directed the NBFCs and other Financial Institutions to refrain from sharing credit information with FinTech companies in September 2019, as sharing of credit information with entities other than Specified User is unauthorized and, since FinTech companies were not categorized as Specified users under Regulation 3 of the CIC Regulations, the FinTech companies were not allowed to access such credit information of customers.

However, the RBI considering the rapid growth of FinTech companies in India and the disruption this limitation will cause in the functioning of the FinTech companies engaged in providing lending services or processing customer-related information, introduced the amendment to bring these FinTech companies under the ambit of Specified Users to allow these FinTech companies to access and process credit information of customers for facilitating CIC. Provided the FinTech company accessing such credit information is eligible to do so.

Eligibility Criteria

1. The company should be incorporated in India or a Statutory Corporation established in India and controlled by resident Indian citizens

2. The company should have a minimum net worth of Rs. 2 crores and shall maintain that all the time and shall have at least 3 years of experience in the business of processing information.

3. The ownership of the company should be well diversified.

4. Neither the company nor any of the promoters/directors of the company should have been convicted of any economic offence or offence including moral turpitude, in past.

5. The company should have a certification from CISA certified auditor that it has a robust and secure Information Technology (IT) system in place for preserving and protecting the data relating to the credit information

The act of the RBI to allow these FinTech companies to access credit information will help the RBI to regulate these FinTech companies in a proper scrutinized manner and the same view was taken by the chairman of the FinTech Governance Council, Mr, Navin Surya.

According to the Chairman of Fin-Tech Governance Council, Mr. Navin Surya, a clearer oversight of users of data and their purpose is now retained. He quotes,-

“With the new framework, companies simply have to register as a specified user with the CICs to obtain data directly. The regulator shall closely watch data integrity and security, helping enforce compliance.”

Moreover, the access to the credit information will help the FinTech companies to increase their turnout time of disbursing loans and credit to its customer since they will be able to take faster, better & more informed decisions for credit writing, as now they have access to more precise credit information to rely on as compared to their previously self-analyzed data of the customer availing credit.

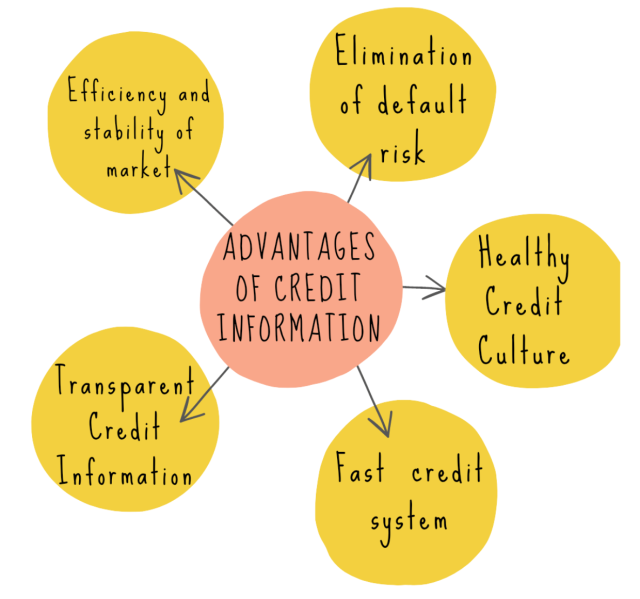

ADVANTAGES

- The sharing of credit information addresses the issue of asymmetric information between borrowers and lenders and helps in increasing the efficiency and stability of the credit market.

- It will help the FinTech companies to eliminate default risks and the new borrowers to get access to credit.

- That Transparency in sharing of credit information will help to promote healthy credit culture by rewarding responsible borrowers and discouraging excessive debt since the credit information report helps both creditors and borrowers as creditors can keep a check on the credit accounts of borrowers and borrowers can monitor their credit scores and guard against pile-up of debt that might become unsustainable.

- The sharing of credit information makes the process of availing of credit fast, secure, and less expensive. It also helps enhance the competition in the credit market.

AMLEGALS REMARKS

The introduction of new regulations will allow FinTech companies to access credit information and become member of the CIC. This categorization of the FinTech companies as Specified Users will assist these companies in the screening of customers and monitoring credit risks more effectively thereby reducing cost and time, default rates, and average interest rates consequentially increasing lending capacity.

Furthermore, the access of the credit information to the FinTech companies will in turn enhance competition, deepening of credit markets and be in a better position to lend by avoiding instances of reckless lending.

That RBI considering the increase in the shift toward digitization and rapid growth of the FinTech sector in India has taken a much-needed step to allow the FinTech to have access to the credit information of customers being Specified Users, as this categorization will lead towards a more liberalized regulatory environment for FinTech companies in India.

This inclusion will further, promote fair play between FinTech and other financial institutions in India and it will benefit not only FinTech companies but will also help consumers since FinTech companies based on the credit reports can now come up with better plans for customers.

For any queries or feedback, please feel free to get in touch with tanmay.banthia@amlegals.com or prarthana@amlegals.com.