INTRODUCTION

In this fast-moving world, user convenience and seamlessness are shifting everything to digitalization. This era of digitalization has an impact on various aspects of our lives including Insurance.

In this new era, the mechanism of availing of Insurance has been completely transformed from the traditional strategy of ‘one size fits all’ Insurance Policies to the introduction of customized and personalized Insurance Policies, based on a precise risk assessment of the consumer, with the help of Internet of Things (“IoT”) connected devices, Artificial Intelligence (“AI”), Big Data analytics and Machine Learning (“ML”).

With the introduction of InsurTech Platforms in India, the business of Insurance has metamorphosed into a different shape altogether. Further, the onset of an unprecedented pandemic of Covid-19 shifting the consumer toward a digital-first mindset has accelerated the growth of InsurTech in India.

In this article, we attempt to discuss the concept of InsurTech, how it is the driving force for the rapid growth of the Insurance Sector in India, and the key legal issues and legal trends in InsurTech in India.

THE CONCEPT

InsurTech companies are considered an entity, which apply technological advancements such as AI, IoT, ML, etc., to the current insurance sector paradigm in order to develop and deliver customer-centric and efficient products at an affordable premium by minimizing the operation cost.

HOW INSURTECH IS DISRUPTING THE TRADITIONAL INSURANCE SECTOR

A. Automating Underwriting

The underwriting process is a crucial process for an Insurance company to evaluate risk and develop products for the consumer but is a very cumbersome, time-consuming, and lengthy process, which reduces the efficiency of the company. However, InsurTech companies with the use of advanced technologies AI algorithms are able to process the customer’s records, reports, and related information in an instantaneous manner to evaluate risks and provide quotations faster than traditional mechanisms.

B. Faster Application Process

In the traditional mechanisms, the approval process for Insurance products would take weeks or even months, which now with the introduction of InsuTech companies has reduced drastically.

The InsurTech companies with the help of advanced technologies and user-friendly mobile applications are able to approve the application process within a matter of minutes since the customers with the help of a user-friendly mobile application can fill out forms from anywhere in the world.

Thereafter, the InsurTech companies with the help of AI algorithms can examine the data to determine whether an applicant qualifies for a given policy or not, allowing these companies to serve a larger pool of consumers at once.

C. Automating the claim process

The Insurance Sector has a bad reputation when it comes to claiming processing or claim management of a consumer, due to its slow administrative process.

However, the InsurTech companies have changed the consumer’s perspective, as InsurTech companies with the help of procurement of data from smart devices or any other source providing a clear picture of the incident are able to process the claim digitally, within a matter of minutes.

D. Micro Insurance or Sachet Insurance

That with the increase in digitization in the field of payments, pharmacy, medical consults, etc., the demand for personalized insurance, Sachet Insurance, or Micro Insurance were increasing rapidly, which the traditional Insurance companies have failed to fulfill.

Nonetheless, the InsurTech companies with the help of advanced technologies are able to automate the underwriting process and conduct a precise risk assessment for developing customized Sachet Insurance Policies or Micro Insurance Policies for consumers, which can be embedded across multiple categories.

E. The introduction of Video Based KYC (“V-CIP”)

The onset of the unprecedented pandemic Covid-19 in 2020 saw businesses undergo tremendous changes, with digitalization being the most significant transformation to suit the changing circumstances.

The Reserve Bank of India (“RBI”) considering the shift towards digitalization vide Circular No. RBI/2019-20/138 dated 09.01.2020 issued an Amendment to the KYC Master Directions allowing banks to conduct the verification of customers’ identity and onboarding process through V-CIP.

With the uncertainty arising from the COVID-19 situation in India, the Insurance Sector with the help of InsurTech companies shifted its presence online to create a niche in the consumer market and reap the rewards.

The Insurance and Regulatory Development Authority of India (“IRDAI”) considering the benefit of digitalization of Insurance services allowed all the Life Insurance and Health Insurance companies to onboard consumers with Video based Customer Identification Process with the help of V-CIP vide circular bearing no. IRDAI/SDD/CIR/MISC/ 245 /09/2020 dated 21.09.2020.

F. Regulatory Support

The IRDAI has played an active role in supporting innovation in the Insurance Sector with the introduction of Regulatory Sandbox in the year 2019 and by permitting the Insurance companies to use V-CIP to onboard consumers.

Thereafter, Government institutions such as the Health Ministry and NITI Aayog have also supported InsurTech companies in India with the introduction of the National Digital Health Mission (“NDHM”), the Digital Information Security in Healthcare Act (“DISHA”), and the National Health Stack, which are aimed at creating an integrated Digital Health infrastructure.

KEY RECENT DEVELOPMENTS

a.) PhonePe entered the InsurTech industry in the year 2020 with a limited insurance ‘corporate agent’ license, allowing it to work with only three insurance firms per category (health, life, and general). However, the IRDAI on 30.08.2021 granted the company a ‘Direct Insurance Broking License’, which will allow the company to deliver a lot more customized products to its users.

b.) The Gujarat International Finance Tec-City (GIFT City) and India InsurTech Association (IIA) on 09.08.2021 entered signed a Memorandum of Understanding (“MoU”) to collaborate closely on several fronts including bringing global insurance companies, Indian insurTech Start-ups, and insurance players to the GIFT City. This association will promote new digital business models and foster collaboration among Start-ups and other Insurance companies.

c.) The IRDAI in the year 2019 introduced the Regulatory Sandbox Regulations 2019 (“IRDAI Sandbox”) to provide a testing environment for new business models, processes & applications, and proposals to experiment and test innovative solutions, which are not explicitly compliant with the existing statutory & regulatory framework.

The IRDAI considering the delay caused due to unprecedented pandemic has extended the IRDAI Sandbox regulation for two years in the year 2021 to allow applicants complete experiments on time and accept the submission of new sandbox proposals.

LEGAL ROADBLOCKS FOR INSURTECH COMPANIES

1. Data Protection

It is an evident fact that InsurTech companies are highly dependent on the data of the consumer acquired by the company with the help of advanced technologies, to evaluate risk and develop products.

Data breaches and cyber-attacks have become quite rampant in the FinTech sector in India. As per reports from the Ministry of Electronics and Information Technology (MEITY), nearly seven lakh cases of cyber-attacks were reported until August 2020, which shows Fintech sector is not immune from the dangers of Cybersecurity, given the fact that the FinTech sector has mostly benefitted from the unrestricted flow of data. Therefore, data protection is of paramount importance for FinTech players in India.

Cyber security risks involve Third-Party Security Threats, Data Breaches, Cloud-Based Security Threats, Digital Identity Risks, etc. Thus, to battle the Cybersecurity threats and prevent hackers from gaining access to sensitive data, there should be a balanced approach to innovation to encourage the FinTech Industry’s growth while mitigating the dangers associated with FinTech services.

However, India currently lacks a standalone codified law, so far as Data Protection and Privacy are concerned. Thus, with regard to Data Protection, the FinTech Industry is primarily governed by the Information Technology Act, 2000 and the Information Technology Rules, 2011.

2. Smart contracts and Blockchain

The issues concerning the timely settlement of InsurTech companies can be speedup with the help of an infusion of Smart Contracts and Blockchain Technology, which allow ordinary contracts to be converted into computer code, removing the need for time-consuming authorization and validation procedures. However, India currently lacks a robust regulatory framework with respect to Smart contracts and blockchain technology.

3. Intellectual Property

When it comes to the use of connected devices and advanced technology, it is also important to ensure whether these technologies are protected under the regulatory ambit of intellectual property rights (“IPR”). Since, whenever a new technology is developed internally, obtained, or licensed from a third party, extra caution is required when it comes to underlying IPRs.

Furthermore, the underlying software policies and architectures are constantly required to be reviewed, including which type of open source software is used in order to ensure that there will be no issues in the future and that the same software will be supported by an adequate community, which is also important for cybersecurity compliance.

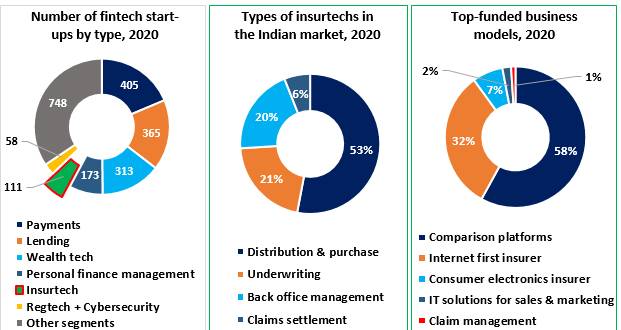

THE PAST DEVELOPMENT

The InsurTech companies i.e., the technology-driven insurance Start-ups have emerged as a major attraction for investors between the year 2015 and the year 2020 –

THE FUTURE PERCEPTION

To survive the changing time and increasing demands, Insurance Sector has experienced heavy pressure to adopt technologies that were considered risky, initially, to survive the market. Simultaneously, the pandemic played a catalyst in adopting new technologies in the insurance sector.

Based on the World InsurTech Report, 2022 the global InsurTech service market is predicted to increase at a compound annual growth rate (CAGR) of 29.2 percent from $8.07 billion in 2021 to $10.42 billion in 2022. The reversal in growth trajectory is primarily due to enterprises stabilizing their output following the COVID-19 epidemic in 2021 when demand rose rapidly. At a CAGR of 30%, the market is estimated to reach $29.75 billion in 2026.

Therefore, considering the growth InsuTech companies have witnessed over the past years and the future perception mentioned above, the future for InsurTech is surely bright in India provided that Insurance Companies adopt a more technology-driven approach and at the same time, legal recognition of such technologies and a robust regulatory framework with a proper complaint redressal forum, will facilitate the growth of InsurTech companies in India,

AMLEGALS Remarks

With the rapid shift towards digitalization, change in consumer behavior, user convenience, and regulatory support the InsurTech companies over the years has witnessed exponential growth and the perception that the insurance business is ready for innovation and disruption is driving venture capitalist and other big players to invest in the Insurance Sector in India.

As evident from above, the InsurTech Sector has seen a substantial and direct beneficiary of the rapid digitization and globalization of the Indian economy. However, the benefits of such a massive shift towards digital financial markets have also brought along the increased risks associated with rampant cyber security attacks, data breaches, etc.

These risks become even more pronounced in the absence of a specific, exhaustive, and stand-alone legislation on Data Privacy in India. GDPR, with the example it has set globally, has influenced the upcoming PDP Bill to a very large degree. In particular, the importance of Data Localization.

In order to keep the current streak of growth going, players in the FinTech sector must ensure that they make continuous efforts with the help of data privacy policies and measures since cybercrimes and cyber-attacks can potentially cause several hindrances to the FinTech market.

For any query or feedback, please feel free to connect with tanmay.banthia@amlegals.com or prarthana@amlegals.com.