INTRODUCTION

The Financial Services player currently views Smart Contracts and Distributed Ledger Technology (hereinafter abbreviated as “DLT” for the sake of brevity) as the way forward for a secured, efficient and rapid growth of the FinTech Sector in India.

The interplay between Smart Contracts and DLT will help in the growth of the FinTech Sector in India since the contract forms the backbone of any professional relationship that an organization develops during its lifetime. Therefore, contracts play an essential role towards the advancement of liberal market relations of a company.

Further, after the introduction of Big Data and Artificial intelligence, Smart Contracts with the help of DTL have made their way towards emergence of a new era of contractual relationships, which has imposed an impeding challenge on the understanding of current regulation governing contractual relationships in India i.e., Contract Law.

The concept of Smart Contract offers a wide spectrum of uses, from Real Estate, Health, Trade Finance, P2P Finance, Insurance, Financial Services etc. However, these innovations are essentially in their infant stage and there is no consensus as to what a Smart Contract is, what function it may serve in the market, or how it will engage with established legal norms and paperwork.

However, these innovations are essentially in their infancy, and there is no consensus as to what a smart contract is, what function it may serve in the market, or how it will engage with established legal norms and paperwork. Therefore, India faces a lengthy technological and legal path ahead of it.

In this article, we attempt to discuss about the concept of Smart Contract and DLT, the challenges, the legal aspect and how the interplay between Smart Contract and DLT will transform the FinTech Sector in India.

SMART CONTRACT

Nick Szabo, a lawyer and developer, initially introduced the concept of Smart Contracts in 1997. Smart Contracts, according to Szabo, are contractual provisions integrated in technology and computer programmes that make breaching them more burdensome

Smart Contracts are essentially computerized algorithm that automatically performs the terms of the contract once the predefined terms stored on the Distributed Ledger Technology are satisfied. The general objectives of Smart Contract is to execute common contractual conditions such as (payment terms, liens, confidentiality, and even enforcement), minimize exceptions both malicious and accidental, and minimize the need for trusted intermediaries.

Features of Smart Contract

1. Tamper Proof

First and the most defining characteristic of a Smart Contract is that it is Tamper Proof. It is not only positively automated to self-operated but also negatively automated to preclude any external influence. The contracting parties need not be under the fear of trusting the other party to perform the obligations or any intermediary to secure performance. The performance of the contract is inevitable.

2. Self-Enforcing

The second feature of Smart Contracts is that they are designed to be and are in fact Self-Enforcing. Smart Contracts do not admit any legal oversight. Pursuant to independent normative, once the predetermined terms decided by the contracting parties are satisfied, the contract will be executed.

DISTRIBUTED LEDGER TECHNOLOGY

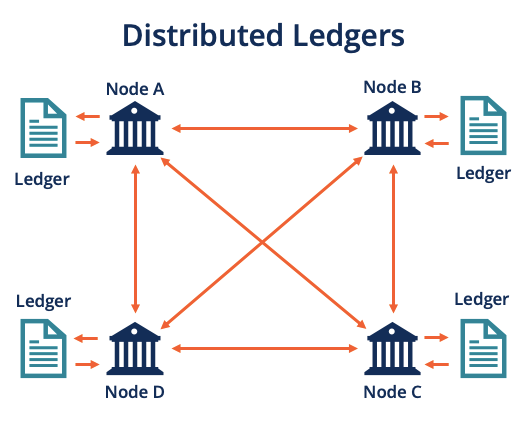

The Distributed Ledger Technology also referred to as Blockchain Technology is a digital database, wherein the data stored is shared across a network of computers (nodes), which is spread across multiple locations allowing its user to simultaneously access, validate, and update the data in an instantaneous manner at the same time.

Under this infrastructure, in order to add new data to the ledger, each node of the network needs to verify and validate the same, thereby creating a robust and secured verification system and eliminating the requirement of an intermediary to verify the transaction. Further, the data stored on DLT is secured, tamper-proof and highly transparent, since the data stored in the digital ledger is etched in time as it can never be deleted or modified, thereby creating a highly reliable and secured system.

Features of Distributed Ledger Technology

1. Decentralized – The process of adding a new block to the database/ledger is governed by a consensus mechanism, where the different nodes on the network participate in the process of deciding whether to add a new block of transactions to the database or not. This decentralized nature of the DLT (resulting from it being controlled by a group of nodes rather than a single central authority) makes it more secure for the participants since the characteristics of the network cannot be changed by a single entity for its benefit.

2. Distributed – Each node keeps a copy of the database/ledger containing details of all the past entries. While this creates redundancy in the network, it also provides security to avoid the manipulation of records. Specifically, any attempt to corrupt the network (by a hacker) may happen only if the data stored on the majority of the nodes in the network is altered.

3. Immutable – Once an entry has been added to the digital ledger, it is nearly impossible to edit, correct, or delete the entry. This makes the data record of past transactions on a DLT almost permanent and unalterable. An entry can only be updated by adding a new block instead of changing/deleting the past record.

4. Secure – The process of adding a block to the database involves cryptography (a mathematical algorithm to encode information for security purposes) and economic incentive mechanisms, which do not require trusting the other nodes involved in the network. This is the emergent property of maintaining a distributed and decentralized database by involving a consensus mechanism. The absence of the need to trust the other nodes involved creates an opportunity to transact and interact with greater confidence.

LEGAL ASPECTS OF SMART CONTRACT

A. Scenario under Current Regulations –

Since these technologies are in a nascent stage, there is no legislation in place that specifically govern Smart Contracts and DLT.

Different types of contracts have different conditions that need to be fulfilled. The contracts covered above are all written and signed. Smart contracts may fulfill the basic condition of offer, acceptance, lawful consideration, and object, however, they are coded which makes it difficult to determine their legality and enforceability.

In light of various specific laws prevalent in India, the situation and analysis of Smart Contracts is as follows:

1. Indian Contract Act, 1872

A contract is valid and enforceable in India only when it casts out the required requisites of a valid contract as enumerated in the Indian Contract Act, 1872.

There are four basic essentials that should be met under the Indian Contract Act. They are as follows:

- one of the parties to the contract should make a proposal to contract, and the other party(s) should embrace that proposal;

- there has to be ‘consideration’ for the proposal, which is some type of worth that should be transferred;

- the stakeholders should have a clear intent to establish legal links; and

- the terms of the contract ought to be definite.

Further, Section 10 of the Indian Contract Act provides that an agreement, which is made by the free consent of the competent parties for a lawful consideration with a lawful object is a valid contract.

Smart contracts fulfill all the basic criteria and do not contravene any clause of the Indian Contract Act. Thus, it can be considered a proper and valid contract under the Indian Contract Act.

2. Information Technology Act, 2000

Information Technology (“IT”) Act, 2000 deals with digital signatures for authentication and usage of any documentary evidence. The act puts forward that in case a document or information is furnished, the same needs to be authenticated by affixing signatures, and then only it can be considered to be a valid document or information.

Smart contracts use cryptography for coding which usually uses digital signatures for authentication and security. The point of concern arises in a case, the signatures produced through blockchain technology is a self-generated. The IT Act does not validate such digital signature produced through one’s own software.

Thus, all the documents or information for which authentication is required can be produced by the Smart Contracts but they are not certified by the IT Act and hence their authenticity can be questioned.

B. Enforceability

Whilst smart contracts are considered to be fully integrated with the existing contract law, it might also lead to a beginning of the end of contract law. Smart contracts may not be considered contracts in the real sense but rather an automated programme that can be used to warranty the performance of terms.

Smart contracts are not synonymous with a legally binding contract. Smart contracts are used for developing applications that may have only a little connection to a legally binding contract, such as supply chain management, identity management, etc. However, this does not imply that Smart Contracts can never constitute a part of a legally binding contract.

A Smart Contract would be deemed valid as a contract by national courts or tribunals only if it fulfills all the essential elements of a contract stated above. Further, a Smart Contract should not only be legal but also enforceable by law.

Further, with respect to the application of law and jurisdiction, as the data on DLT exists on a network of computers with nodes and users typically based all over the world.

Generally, the parties to the smart contract can contractually choose the law applicable to the contract. If the contracting parties have expressly opted for the law of a particular nation or if the court finds from the terms of the contract that the parties intended to have the law of a particular jurisdiction applicable, the court will apply the right and duties applicable in that jurisdiction.

Nonetheless, the choice of the law selected to govern the smart legal contract should take into account the DLT design, the business aspect, technical complexity, number of participants, scope of jurisdiction, and other relevant factors.

C. Dispute Resolution

Since smart contracts are self-enforceable, it should not be misunderstood that there is no need to consider dispute resolution mechanisms based on the misconception that disputes will not arise.

There are many possible scenarios where dispute might arise with respect to issues pertaining to (but not limited to) – fraudulent and/or negligent misrepresentation, mistake of law or fact, the contract being void for illegality, coding errors, etc.

Arbitration has certain characteristic features based on which it can naturally be opted to resolve disputes arising out of smart contracts.

Firstly, Smart Contracts disputes will usually involve witnesses and expert evidence with sensitive information pertaining to the new technology that parties intend to keep confidential. In many jurisdictions, there is a mandatory obligation for the parties to maintain confidentiality, meaning that the documents disclosed or used in the arbitration cannot be disclosed or used for any other purpose.

Thus, arbitrating Smart Contracts disputes would be advantageous for parties who do not want their exclusive business information to become public.

Secondly, since Smart Contracts use blockchain technology vis a distributed ledger network of computers, it would be difficult for the courts to determine whether it has jurisdiction over the dispute or not and what is the governing law of the smart contract if not decided by the parties.

An agreement to arbitrate the smart contract disputes removes the uncertainty and risk involved in litigating the dispute.

ISSUES RELATED TO SMART CONTRACTS

- Firstly, the Smart Contract’s inability to address contingencies. For instance, provisions with respect to the frustration of contracts due to change of law, impossibility, Force Majeure, and Act of God, etc., can be built into traditional contracts but may not be possible in smart contracts.

- Secondly, the immutability and irreversibility of such contracts could be a challenge. Under contract law, a contract is not just a set of instructions to be automatically executed; rather they are interpreted in the context of ever-changing real scenarios. Spirit of law supersedes the letter.

- Thirdly, Under the existing provisions, contracts need signatures. Similarly, digital signatures are required for contracts that are executed digitally. The Indian IT Act, 2000 puts a limitation on obtaining these digital signatures and says that only a government-designated certifying authority can provide these signatures. This conflicts with blockchain technology as it uses a hash-key for authorization.

- Fourthly, certain terms in a Smart Contracts for example ‘reasonableness’ may not be considered by a computer code because a code is entirely based on objective consideration.

- Fifthly, in certain transactions in Smart Contracts with regards to land and another asset, the asset is tokenized and sold to the buyer using a computer code. However, this may not be permissible in the substantive law regarding the sale of an asset where the sale must be witnessed and sold through a deed.

BENEFITS OF SMART CONTRACTS

Smart contracts are really beneficial for FinTech players. The anticipated potential is almost limitless, that is, it would transform law, finance, and civil society. It is construed to be a ‘mature end of the evolution of electronic agreements over several decades.’

Public smart contracts are beneficial in a wide variety of commercial applications due to their ease of deployment. Whereas the permissioned smart contracts are beneficial for collaborative business processes as they would help in preventing unwanted updates, improve efficiency and save costs.

In the short term, it will definitely have a subtle and meaningful impact to the extent of enhancing the efficiency, transparency, and granular control in the contracting regime by limiting intermediation and operational interference.

1. Ability to Reduce Adverse Selection

The problem of adverse selection is commonly observed in many transactions, meaning that the asymmetry in information during the search and negotiation phases of a contract induces risks and cuts down the potential profits for all participants even before the transaction is agreed on.

The advent of the era of smart contracts in the market would reduce the risk by ensuring that there is no ambiguity through the iterative design and reliance on logical equations.

As mentioned earlier, all the member of the particular blockchain network has the access to the entire record of all the transaction, including previous transactions and the addended ones.

This facilitates the agents to analyze and review the history of the potential trading partners without the need to rely only on their reputation or recommendation. Understanding the past behaviors will pertinently be beneficial for growing businesses like start-ups.

The Smart Contracts further reduce any sort of risk involved in a transaction by performing the function of an escrow (An authorized independent party that is entrusted to hold the assets until certain conditions are fulfilled).

Smart Contracts not only reduce the cost of a custodian or government agency but also eliminates all privacy concerns. It stores information and digital assets directly on the blockchain and acts an anonymous channel between the parties.

2. Ability to Reduce Moral Hazard

Issues pertaining to moral hazard usually occur after the transaction has taken place. It is basically the inability to observe the other parties’ actions ex-post the transaction. This might often arise when the agent has the motive to withhold the information or act against the interest of the principle.

In a paper-based traditional contract, the cost of supervising and examing the behavior of the agent is too high. However, Smart Contracts, permit the verification of certain actions through the use of proofs through oracles. Further security for confirmation can be obtained through the use of additional oracles. Thus, the possibility of moral hazard is reduced or to an extent removed completely.

Correctly designed smart contracts aid in better surveillance of the execution of the transaction and significantly reduces the cost. Costs would be only limited to transactions that requires technical expertise and where verification takes place off-chain.

Owning to the operations of proofs of existence and oracles, smart contracts allows the contracting party to implement and verify governance protocols and complex agreements with ease that otherwise are difficult or impossible to verify.

Further, Smart Contracts can curb the negative effect of moral hazard by virtue of the binary design of the blockchain technology that ensures it is not ambiguous.

Smart contracts are not prone to complexities of interpretation that are present in traditional contracts as it based on contemporary legal language which is usually open for interpretation. Linguistic obscurities are removed significantly and thus potential legal disputes are reduced.

The coded contract is executed by blockchain precisely as it was agreed on, eliminating the requirement to trust or be dependent on other contracting parties.

3. Efficiency through Automation

The primary and basic contribution of smart contracts over traditional contracts is that the former is based on the use of digital computing power that increases the performance and also execution efficiency through automation.

The feature can specifically be a worthy option when a large number of the similar transaction take place between the users within a network and transactions are based on a manual or are being duplicated.

Considering that smart contracts can automate and scape them up almost infinitely, they have the ability to enhance the speed of many business processes. This especially would be valuable for the finance sector wherein multiple transactions take place within a fraction of seconds.

4. Internet of Things

Smart contracts can also be applied to physical products connected to the web, known as the Internet of Things. This association will help in the reduction of transaction costs.

Smart contracts can trigger a fast, safe and transparent transfer of property ownership, known as the smart property. As discussed above, smart contracts eliminate the requirement of a middleman to handle the transfers and property ownership as now it can be done to anyone anywhere around the world.

One of the leading companies engaged in the application of Smart Contracts to the internet of things is IBM. IBM is in the process of designing radio-frequency identification chips, barcode scanners, and similar devices to transfer data to the DLT to verify and append the smart contracts. Following is an illustration of how the process functions:

As the package connects to the Internet of Things and move along various distribution centers, the location of the package and other information will be updated on the blockchain. This facilitates all the parties to be informed about the status of the package as it moves among various parties and be assured that the terms of the contract are fulfilled.

5. Simplified Compliance

The development of blockchain technology and smart contracts will further help in efficient compliance with regulatory measures. This is covered under the category of “RegTech” wherein innovative technology is used to tackle regulatory issues in the finance sector.

Smart contracts are aimed to be coded to commence automatic compliance with specific regulations or intra-organizational compliance rules. Further, considering the fact that smart contracts are stored in a distributed ledger, an indefinite financial audit track would be recorded for any interested person, like supervisors and regulators, to look on.

The use of RegTech will further especially be beneficial for the finance industry as the technology would be a huge measure towards reducing regulatory and compliance costs. This will not only help the established financial institutions but also the smaller banks and financial startups. However, a major hurdle is the willingness of regulators to authorize them.

AMLEGALS Remarks

There are legitimate reasons for players of the TCL (Techno Commercial Legal) Industries and FinTech Industries to be both optimistic and pessimistic about the emergent manifestation of Smart Contracts.

As discussed above, Smart Contracts have the potential to increase commercial efficiency, reduce transaction and legal costs, and facilitate transparent and anonymous transacting. There are, however, issues pertaining to the legal enforceability of Smart Contracts. It is still not certain whether Smart Contracts will easily adapt to current legal frameworks regulating conventional contracts across jurisdictions.

At this moment, it is too early to predict how authorities will react to Smart Contracts since these innovations have not matured to the degree to which they require legislative intervention.

However, with time, as Smart Contracts become more widely used and applied in a larger variety of commercial use, it is essential that the law keep pace as otherwise, uncertainty would be the propagating ground for the disputation.

-Team AMLEGALS assisted by Ms. Deepali Maheshwari (Intern)

For any queries or feedback, please feel free to get in touch with tanmay.banthia@amlegals.com or prarthana@amlegals.com.