INTRODUCTION

MSMEs or Micro, Small and Medium Enterprises are one of the key players in the market and contribute immensely to the Indian economy. They contribute to about 37.5 % of the GDP and provide employment to about 117.1 million people.

However, a significant inadequacy exists in financing facilities for MSMEs. Slow-paying Invoices are the major obstacle faced by MSMEs to convert the trade receivables into liquid funds. To bridge this gap, the Reserve Bank of India (RBI) established the Trade Receivables Discounting System or TReDS. It aims to facilitate easy and feasible financial trading from corporate to various buyers including the Government Departments and the Public Sector Undertakings (PSUs).

However, this electronic billing system has deep roots. The initiative is an outcome of the report ‘Hundred Small Steps’ by the Financial Sector Reforms (FSR) Committee, 2008. Pursuant to the recommendation of FSR, Small Industries Development Bank of India (SIDBI), in collaboration with the National Stock Exchange (NSE), undertook the initiative of setting up an E-discounting platform so as to support finance receivables known as NTREES (Trade Receivables Engine for E-discounting, where N stands for NSE and S for SIDBI).

WHAT IS TReDS?

TReDS or Trade Receivables Discounting System is an initiative by RBI to facilitate the MSMEs in financing of trade receivables. This system not only discounts invoices, but also the bills of exchange.

The platform enables MSMEs to receive payments on scheduled time while also allowing corporate buyers to extend credit terms up to 180 days, aligning their cash flows and obtaining a better discounted rate. This allows buyers and their MSME suppliers to better manage their working capital cycles, resulting in significant cost savings.

TReDS transactions are to be executed without recourse to the MSMEs, thus, providing a greater benefit to the MSMEs. These transactions can be initiated by both the MSME supplier as well as the buyer. MSMEs have easier access to capital at lower rates, without having to put up any additional collateral.

WHAT IS INVOICE DISCOUNTING?

The practise of utilising a company’s unpaid accounts receivable as collateral for a loan given by a finance company is known as Invoice Discounting. Borrowing through invoice discounting is for a very short time period, as the amount due can change as soon as the quantity of the accounts receivable collateral changes.

Invoice discounting essentially speeds up cash flow from customers by allowing you to collect cash almost as soon as the invoice is issued, rather than waiting for clients to pay within their standard credit terms.

There are four types of invoice discounting:

- Confidential invoice discounting: It is a confidentially negotiated invoice, also known as undisclosed invoice finance which takes place without the knowledge of the buyer. Only the supplier has access to these invoices. Though these invoices are costlier than the disclosed invoices but the trust degree between the supplier and the buyer is very high due to confidentiality.

- Disclosed invoice financing: Unlike confidential invoice discounting, both the supplier as well as the buyer are aware about the transaction under disclosed invoice financing. A direct transaction between the buyer and financer takes place without involvement of any intermediary.

- Spot invoice discounting: These invoices are sold on an individual basis and are ideal for small businesses whose funds keep fluctuating.

- Whole turnover invoice discounting: The process of selling a full sales ledger is known as Whole Turnover Invoice Discounting. This is ideal for long term businesses where dealing takes place in wholesale or in case of long-term contracts.

HOW DOES INVOICE DISCOUNTING WORK?

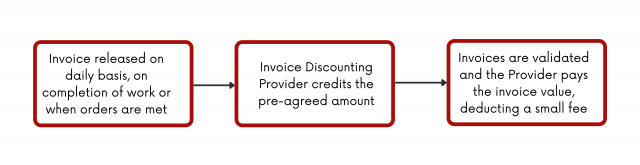

The invoices are released on a daily basis on completion of work or when orders are met. Pursuant to receiving the invoice, an invoice discounting provider credits the pre-agreed amount. After establishing that the invoices are valid, the provider pays the value of the raised bills, deducting a tiny percentage.

Since it is a system where cash flows are made daily, daily release of invoices is crucial. Once the clients have paid the MSME, the discounting company has to be refunded the loan plus an agreed-upon charge to cover costs, risk, and interest. The cost is normally between 1% and 3% of the entire invoice amount.

WHY INVOICE DISCOUNTING?

Invoice discounting ensures quick payments since the cash flow is accelerated. It is monetarily feasible as it is cheaper than a bank loan. The process eases conducting business and even helps in the future planning of the business. Further, the money acquired by invoice discounting could be used in a variety of ways, including hiring temporary workers during a busy season, purchasing more goods or raw materials, getting through a poor business time, or investing for the future.

INTERPLAY OF TReDS AND INVOICE DISCOUNTING

On TReDS, invoice discounting involves three parties: the MSME Supplier, the Corporate Buyer, and the Financier. Depending on the manner of discounting, either the buyer or the supplier uploads the invoice, which is then accepted by the other side.

When the invoice is accepted, the platform’s financiers begin bidding on it. The supplier accepts the bid, and the discounted amount is credited to its account T+1 day after acceptance, where T is the acceptance date.

In the times of COVID-19 pandemic, this has proven to be the best resort for MSMEs to curtail the difficulties of acquiring funds. With the increased utilisation of TReDS, Mynd Solutions (M1 Exchange), TReDS Ltd. (Invoice mart) and Receivables Exchange of India Ltd. (RXIL) have been granted the license by RBI to operate as TReDS platform.

REGULATORY FRAMEWORK FOR TReDS

The RBI has issued Guidelines on TReDS on 3rd December, 2014. The Guidelines provide the Scheme for setting up and operating the Platform, its participants, process flow and procedure, settlement procedure and regulatory framework. Subsequently, the RBI granted in-principle approval to SIDBI and NSICL for establishment and operation of the TReDS platform in conformity with the RBI Guidelines on TReDS and the Payments and Settlement System Act, 2007.

The Department of Micro, Small and Medium Enterprises vide Notification bearing S.O. 5621(E) dated 02nd November, 2018, directed all companies registered under the Companies Act, 2013, and having a turnover of more than INR 500 Crores; and all Central Public Sector Enterprises; to mandatorily onboard a TReDS Platform. Therefore, TReDS registration is a mandatory compliance for the abovementioned companies. Further, the Registrar of Companies of each State is appointed as the Competent Authority to ensure and monitor compliance with the Notification.

AMLEGALS REMARKS

In India, digitization in the financial industry has made the process of obtaining credit through invoice discounting much easier. MSMEs can now obtain funding without much hindrance and difficulty, thanks to this financing alternative. TReDS, an online financing platform, was established to augment the benefits of invoice financing.

RBI has permitted only three entities to perform the functions of a TReDS Platform and provide Invoice Discounting, thus, indicating that such platforms are heavily regulated and such financing cannot be provided by any unregulated financier. Hence, it is anticipated that TReDS platforms will facilitate MSME financing, along with ensuring strict compliance with legal and regulatory requirements.

TReDS has been praised by many as a crucial initiative in India’s financial industry, and it is projected to significantly stimulate MSME growth. Along with incorporating and facilitating invoice discounting mechanism, it has strengthened the MSMEs, thus, contributing to strengthening of the Indian economy.

This initiative is a flexible, speedy and trustworthy model as it is buyer centric and it mandates acceptance of invoices by the buyer, thus, mitigating the chances of any default.

For any query or feedback, please feel free to connect with rohit.lalwani@amlegals.com or mridusha.guha@amlegals.com.