INTRODUCTION

India has always been inclined towards the use of cash for financial transactions. However, with rapid development of the technology, accessibility of the internet coupled with government initiatives such as ‘Digital India’, everything is shifting towards digitalization and this era of digitalization has an impact on various aspects of our lives including finance.

The term FinTech has always been around. However, the technological advances, change in demand for financial products, and competition in Financial Service Sector has led to redefining of the business models across different segments of the Financial Services industry by enabling them to improve service delivery systems which in turn is contributing towards digital financial inclusions.

Fintech, as the word suggests, is a fusion of “Financial services” and “Technology” and refers to those companies, which use technology to automate and enhance procedures of providing financial services in an efficient and faster manner.

FINTECH LANDSCAPE IN INDIA

The FinTech industry in India has been growing rapidly due to India’s profound customer demand, diverse capital flows, strong tech talent, and enabling framework policy. Currently, the FinTech players are redefining the business models across different segments of the Financial Services industry including lending, wealth management, insurance, digital payments, regulations, capital markets, supervision, and underlying enabling techs.

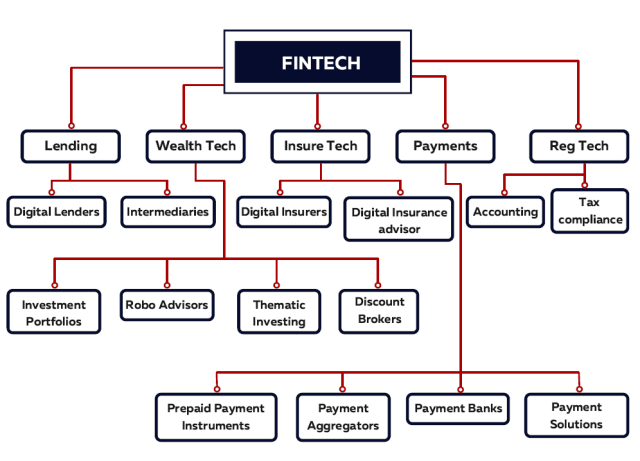

The FinTech market in India can be broadly categorized into the following:

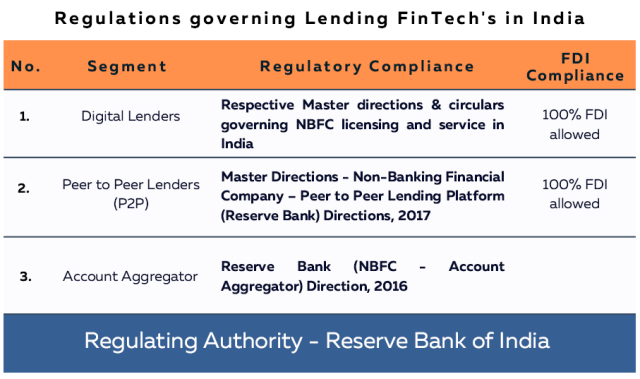

1. Lending

Lending can be broadly categorized into two key segments – digital lending and intermediaries.

a. Digital Lending

The introduction of the Digital Lending Platform has metamorphosed the business of lending into a different shape altogether.

It is the platform where everything is happening from capturing personal and professional data of the Borrower, use of credit engine to check credit history, creation of a proposal for user, acceptance, and execution of legal documents, e-KYC, online disbursement, and repayment of the loan within a matter of minutes.

The process is virtually now instantaneous and all it takes is 3 minutes to think, 1 minute to transfer, and 0 human touch.

- Retail Lending

This segment focuses on providing credit directly to the consumers through a Digital Platform and usually involves services such as personal loans, loans against salary/payday loans, gold loans, pay later loans, etc.

- Merchant Lending

This segment focuses on providing credit directly to the business through a Digital Platform and usually involves services such as invoice discounting, Trade Receivable Discounting systems, SME lending, channel finance, credit scoring, etc.

b. Intermediaries

Intermediaries can be broadly categorised into two key segments – P2P Platforms and Aggregators.

- P2P Platforms

P2P lending is a platform-based lending mechanism that connects lenders directly with market-based creditors. This puts together various classes of creditors and lenders on a common forum and then analyses the desires and requirements of all parties to facilitate a deal that is ideally tailored to both.

- Aggregator

Account Aggregator is an entity that is engaged in the activity of financial data aggregation, under which it gathers financial information as defined under Section 3 (ix) of NBFC-AA Direction, 2016 (“The Regulation”) of the Customer on a single platform and then shares it with the explicit consent of the user with the financial information user via Open Application User Interface (API).

2. Wealth Tech

Wealth Tech is a platform which uses technology to provide wealth management services to its users. The primary goal of Wealth Tech is to provide innovative digital solutions for the investment and asset management industries. This platform uses technology such as Artificial Intelligence (AI) and Big Data Analytics to transform traditional wealth management and investment services.

Wealth Tech comprises of products and services offerings ranging from financial services software, investment platforms, online investing tools, and robo-advisors to digital brokerages.

The Wealth Tech Segment majorly includes the following:

a. Investment Platform

This Platform allows its users to buy, sell or hold funds securely without intervention of a middleman or a broker. The user can invest directly on a non-advised basis via a D2C (direct to customer) platform, or on an advised basis using a financial adviser who will invest on your behalf.

b. Robo-Advisor

This is the most famous Wealth Tech Technology. This platform works as an automated service that provides profitable investment options and yields targets to its users based on risk appetite, age, income, requirements, goals, etc.

c. Thematic Investing

This is an investment philosophy/strategy which analyses broad macroeconomic trends to take advantage of the shifts by identifying and investing in companies that are most likely to benefit from such changes.

d. Digital Discount Brokers

Digital Discount Broker is a platform which helps its users to buy and sell orders at an extremely low or flat brokerage as compared to traditional brokers who charge a percentage of the transaction size.

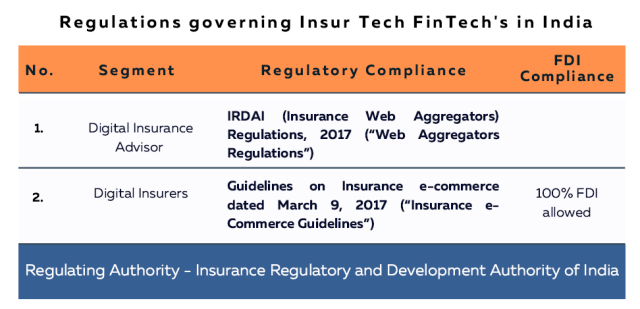

3. Insur Tech

Insur Tech is a digital platform which allows its users to research, compare policies, make a purchase, process claims, handle policies, and a lot more through these Platforms. Insur Tech is transforming the Insurance Industry by reducing cost, improving efficiency, and enhancing customer satisfaction.

The Insur Tech Segment majorly includes the following:

a. Digital Insurance Advisor

This is a web aggregator platform that allows its customers to search, compare, find and buy insurance products at affordable premiums from multiple carriers on a single platform.

b. Digital Insurers

This is a digital platform which offers insurance policies to its consumers at the time of purchase of a product, which allows it to gain access to a wide range of e-commerce consumers. Further, it allows its consumers to initiate, process, handle, and settlement of claims digitally in an instantaneous manner, which enhances overall customer satisfaction and efficiency.

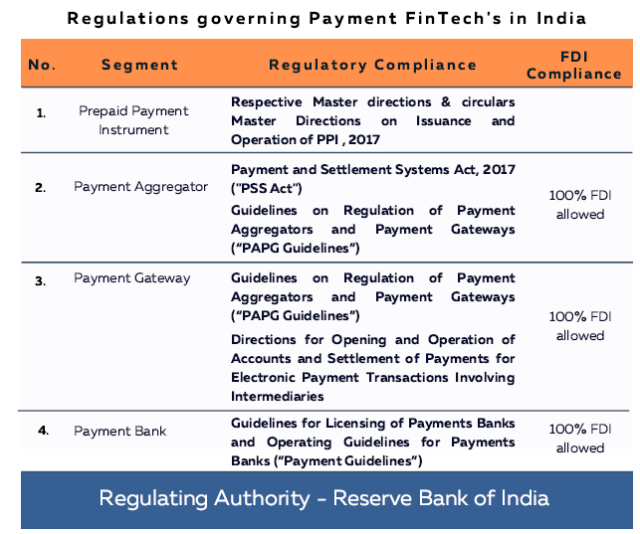

4. Paymnets

Digital Payment is the method in which people send and receive money in their account instantly through a digital mode. The FinTech Companies providing Digital Payment mechanisms have been the torchbearer for the revolution of FinTech Industries in India.

The world has been shifting towards Digital means for quite a long time now however, the dire need for overall digitization was realized in the year 2020 as a result of unprecedented Pandemic. Therefore, the Government of India has been hell-bent on promoting and developing Digital Payment mechanisms in India.

The Payment Segment majorly includes the following:

a. Prepaid Payment Instrument

Prepaid Payment Instruments (PPIs) are the instruments which allows its user to purchase goods and services and avail financial and remittance services against the value “Stored” in them.

The values stored in these Instruments represent the amount of money stored in them that can be used through mode of cash, card, mobile wallets, smart cards, vouchers, etc. In India PPI’s can be issued by Banks and Non-Banking entities as prepaid cards or digital wallets.

The PPI can be classified into –

- Open System PPI

These are the PPIs, which can be issued by the banks authorized by the Reserve Bank of India only. Now, these PPIs can be used by any Merchant for purchase of goods and services, cash withdrawal, payment, remittance services, transfer of funds, etc.

- Semi-Closed System PPI

These are PPIs, which can be issued by Reserve Bank authorized Entity i.e. (Banks or Non-Banks) only for the purchase of goods and services, payment, remittance services, transfer of funds, etc.

However, these PPIs cannot be used to withdraw Cash irrespective of the fact that whether Banks or Non-Banking Entities have issued it.

Further, these PPIs can be used only at those places, where Issuer Entity has entered into specific contracts (through a Payment Aggregator or Payment Gateway) with different Merchants to use these PPIs.

- Closed System PPI

These are PPIs, which can be issued by any Entity for the purchase of goods and services. However, it cannot be used for any Cash transaction, Cash Withdrawal, or payment for Third Party Services irrespective of the fact that whether Banks or Non-Banking Entities have issued it.

Therefore, these types of PPIs are not required to be authorized by the Reserve Bank of India for usage. Further, these PPIs are valid only against the Entity that issued it. Therefore, customers will not be able to use it against any other Entity.

b. Payment Aggregators (Mobile & Digital Wallets)

Digital Wallets is a software based system which allows its users to store money on it like a virtual Pre-Paid Card to conduct transactions electronically. It allows its users to link their bank accounts, Credit card or Debit Card to make transactions in an easy, effortless manner.

c. Payment Gateway

Payment Gateway is the technology used by merchants to collect payment from its customer directly on their website through digital means. The Payment Gateway is the means which keeps the functioning of payment ecosystem smooth between merchant and its customer.

d. Payment Bank

Payment Bank is a new category of Bank introduced by RBI, which can be operated digitally but on a much smaller scale than an actual traditional bank. These banks provide most of the traditional banking services but cannot provide loans or credit to their users.

5. Reg Tech

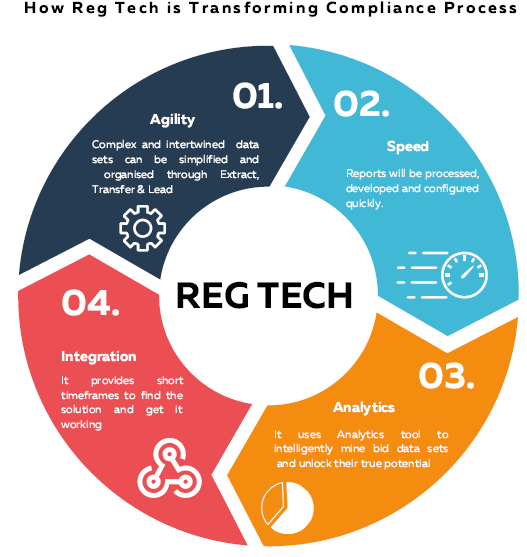

In India, due to the complex nature of Financial industry, it is surrounded by a gamut of regulations. Therefore, in an endeavor to reduce the burden of the regulatory terms, the Financial industry is starting to adapt to the new technology as fast as possible.

Regulatory Technology (Reg Tech) helps businesses to manage complex and tedious regulatory compliances such as e-KYC in onboarding customers. tax assistant, credit scoring, accounting, GST filing, etc., in an efficient manner. Reg Tech has established a solid foundation within the FinTech ecosystem.

GENERAL REGULATORY FRAMEWORK

There are no specific set of laws governing the FinTech industry in India. However, there are certain legislations that govern several aspects of the industry and we shall discuss them hereunder:

1. Payment and Systems Settlements Act, 2007 (PSS Act, 2007)

The Payment and Settlements Act, 2007 essentially governs digital payments within India and prohibits the commencement and operation of a digital payment system without any prior permission or authorization of the RBI. With the diverse FinTech services in India, payment systems like money transfer operations, PPIs, etc. are regulated by the PSS Act, 2007.

2. Information Technology Act, 2000 (IT Act, 2000)

FinTech Companies majorly operate online. Therefore, in order to ensure that they have a secure IT framework in place, the FinTech Companies are required to adhere to the directions set out under Section 43A of the IT Act, which inscribes the responsibility of corporate organizations to pay damages in the event of negligence in maintaining fair security measures for the protection of their users’ private confidential personal data.

3. IT (Reasonable Security Practices and Procedures and Sensitive Personal Data or Information) Rules, 2011 (IT Rules, 2011)

FinTech Companies’ functions rely upon the personal data of their consumers, thus in order to ensure the protection and security of data it is important for the FinTech Companies to comply with the aforesaid rules and formulate a Data Protection Policy of their own to ensure safety of its user data as for the time being India does not have a separate data privacy framework.

4. Prevention of Money Laundering Act, 2002 (PMLA Act, 2002)

The FinTech Companies primarily deal with financial services and products and in order to prohibit these Companies from unlawfully launder money, these Companies are required to comply with the Prevention of Money Laundering Act, 2002 and the Prevention of Money Laundering (Maintenance of Records) Rules, 2005.

5. Foreign Exchange Management Act, 1999 (FEMA Act, 1999)

With FinTech gaining an impulse all over the world, there was a rapid increase in cross-border payment products in foreign currency and as a result, there was a dire need to regulate these cross-border transactions conducted by FinTech Companies in India. Therefore, to regulate the same the FinTech Companies are now required to comply with FEMA.

GENERAL REQUIREMENTS TO SETUP A FINTECH COMPANY

1. Choosing an Appropriate Business Structure

Decide the business structure to set up a FinTech company in India. There are broadly three kinds of business structure pertaining to FinTech in India, namely:

- One Individual Corporation;

- Limited Liability Partnership;

- Private Limited Company;

- Joint Venture;

2. Goods and Service Tax (GST) Registration

Apply for GST registration as GST Registration in India is mandatory for any business which is involved in the supply of goods and services and whose turnover exceeds Rs. 40 lakhs and Rs. 20 lakhs respectively (for Normal Category States) and Rs. 20 lakhs and Rs. 10 lakhs respectively (for Special Category States).

GST Registration requires certain documents such as PAN Card, Aadhaar Card, Proof of business registration, Identity proofs, etc. On completing the registration process, the company shall be allotted a GST Identification Number.

3. Enter into Legal Agreement

Contracts and agreements form the crux of any business and therefore it is extremely important to draft them with due diligence. All the contracts drafted should be as per the provisions of the Indian Contracts Act, 1872.

The Legal Contracts, which are essential for a FinTech company are:

- Intellectual Property Licensing Agreement

- Privacy Policy

- Co-Founder Agreement

- Website User Policy and Terms of Use for mobile users

- Privacy Policy

- Product Development Agreement

- Vendor Agreements

- Employment Agreements

4. Intellectual Property Registration

Intellectual Property (IP) is one of the prime assets of any company which needs to be safeguarded and FinTech Companies are no exception to the same. In order to preserve the sensitive information, goodwill of the brand, mobile apps, trade designs, etc., a FinTech company should necessarily obtain IP protection such as Patent, Trademark, etc., under their respective regulations.

5. Apply for License/NBFC Registration

As discussed above the FinTech Company will have to apply for NBFC registration under the Reserve Bank of India Act or license and licensing of such Companies will totally depend on the type of service that the FinTech shall be offering.

6. Register Domain

It is essential for FinTech Companies to have a presence on the internet. Therefore, FinTech Companies are advised to register their domain and have an established website to broaden their subscribers and customers.

CHALLENGES

1. Lack of Absolute Regulatory Framework

Currently, in India, there is no uniform or umbrella regulation that governs the FinTech industry in India. Therefore, each segment under the FinTech industry has to be regulated depending on the services it is offering as discussed above. Recently, India has become one of the few jurisdictions to have a specific payment and settlement system to regulate digital payment and settlement mechanisms.

However, India has still a long way to go in terms of data privacy, stand on digital currency, investment vehicles, etc. A uniform regulatory framework, a commonly translated language, and standardized KYC norms can open up a vast window of foreign transfers through FinTech’s in India.

2. Data Security

Data breaches and cyber-attacks have become quite rampant in FinTech industry in India. As per reports from the Ministry of Electronics and Information Technology (MEITY), nearly seven lakh cases of cyber-attacks were reported until August 2020. Data protection is of paramount importance for FinTech players and therefore, the need for enforcement of the Data Protection Bill, 2019 in India is more than ever.

3. Restricted Reach

Due to a lack of trust, awareness, and advanced technology the services of the FinTech Companies have been restricted to metro cities alone. This inequality of FinTech services in rural areas acts as a hindrance for these FinTech Companies to grow and increase their consumer base, which in turn hampers the growth of the economy in India.

4. Identification of Platforms

Due to the sudden surge in FinTech opportunities in India, there have been a lot of FinTech Companies participating and providing their services in overlapping spaces, which is making it difficult for the rightful FinTech players to capture market share, increase consumers and growth.

AMLEGALS REMARKS

FinTech Companies have revolutionised the Banking and Financial sector in India owing to their quick, secure, and efficient services. As discussed above, the FinTech industry has been growing rapidly due to India’s profound customer demand, diverse capital flows, strong tech talent, and enabling framework policy.

Over the past few years, Government of India has taken several initiatives to strengthen the FinTech Industry in India such as, “on-tap” licenses to Small Finance Banks, PMJDY, Start-up India, Digital India, Introduction of UPI to include the unbanked population of India in the formal financial services fold etc.

Now, as more and more FinTech players are entering into the Indian market responsibility of these FinTech Companies to maintain a simple, efficient, and secure platform for its consumers has increased multifold, especially in the absence of uniform data security law in India.

Now, FinTech industry in India is still in the early adoption stage. However, considering the investment received in the last few year, we believe it is well-positioned to witness long-term growth in the coming years.

For any queries or feedback, please feel free to get in touch with tanmay.banthia@amlegals.com or prarthana@amlegals.com.