INTRODUCTION

With the rapid growth in digitalization, the business model of Online Bond Platforms (“OBPs”) offering debt securities to its investors, have witnessed an exponential growth over the past few years. In this business model there are mostly FinTech companies or companies backed by Stock brokers/ SEBI registered intermediaries.

The Securities and Exchange Board of India (“SEBI”) considering the rapid growth of OBPs and the risk associated with it, decided that there is need of having checks and balances in place in the form of transparency in operations and disclosures to the investors dealing with such OBPs, measures for mitigation of payment and settlement risk, availability of redress mechanism in case of complaints, etc. in order to safeguard the interest of investors in the bond market.

Thus, the SEBI in order to streamline the operations of these OBPs and to facilitate the participation of investors in the bond market, introduced the Regulatory Framework vide Notification dated 09 November, 2022.

In this article we attempt to discuss about the concept of OBPs, how it works, the need for regulatory framework, the obligation on the OBPs under the guise of the Regulatory Framework, its effect on private placement issued by companies and how it will help in the growth of Bonds market in India.

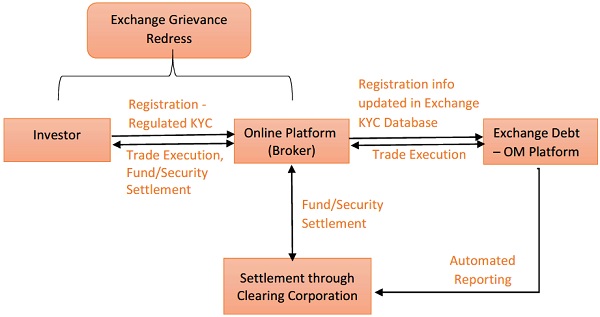

THE CONCEPTThe OBPs are companies, which allows its non-institutional investors to deal in debt securities and these OBPs primarily function on two business models, wherein in one model the OBPs only play the role of platform provider where they empanel brokers who provide inventory on the platform and platform provider charges fee for offering platform and any other services and in the second one, the OBPs provider itself procure bonds either from primary or secondary market and then further sell to participants by adding spread/margin on the price of the bond.

HOW IT WORKS THE NEED FOR REGULATORY FRAMEWORK

THE NEED FOR REGULATORY FRAMEWORK

The OBP over the past few years have witnessed an exponential growth which can be attributed to the following factors:

Firstly, persistently low interest rates in recent years have reduced the appeal of traditional fixed deposits for investors. This has prompted the investors to seek alternative investment options such as debt securities offered on bond platforms.

Secondly, the increasing digitalization and internet penetration have made investors more tech-savvy. The investors are now comfortable using online platforms for various financial transactions, including investing. Bond Platforms capitalize on this trend by providing a convenient and user-friendly interface for investors to purchase a variety of bonds.

Thirdly, the Covid-19 pandemic and subsequent lockdowns have resulted in a significant increase in the number of demat accounts and investors in the securities market. This has created a larger pool of potential investors for bond platforms, Furthermore, bond platforms often offer more attractive returns compared to traditional fixed deposits. This appeals to investors who are seeking higher yields on their investments.

Lastly, bond platforms provide easy access to non-institutional investors for investing in debt securities. These platforms offer a user interface similar to popular online shopping websites like Amazon or Flipkart, making it convenient and familiar to investors to navigate and make investment decisions.

However, it is a well established facts that investments in debt securities are subject to risks and there was no statutory obligation on these platforms because there is no regulatory body governing it. Furthermore, there was no standard method/Process available for the investors to address their grievances unlike trades done through regulated frameworks. Therefore, the SEBI in order to bring in the OBPs within the regulatory ambit and to safeguard the interest of investors, introduced the Regulatory Framework.

THE REGULATORY FRAMEWORK

1. Mandatory Stock Broker Registration: The companies intending to operate as OBPs shall register itself as a stock broker in the debt segment of the Stock Exchange, in lieu of Section 51(A) of the SEBI (Issue and Listing of Non-Convertible Securities) Regulations, 2021.

2. Appointment of Key Managerial Personnel: The OBPs must appoint a Company Secretary as the compliance officer and two Key Managerial Personnel with a minimum of three years of experience in the securities market.

3. Grievance Redressal Mechanism: The OBPs shall have in place a well defined system to address grievances that may arise during the course of business along with authentication from SEBI Complaints Redress System (“SCORES”).

4. Technology Infrastructure: The OBPs must have in place a robust technology infrastructure having high degree of reliability, availability, scalability and security to support its operations, which shall provide real-time dissemination of information to other entities in the system maintaining investor privacy, and ensuring open access to potential investors.

5. Adhere to Know Your Client (“KYC”) Requirement – The OBPs shall abide by the KYC Directions issued by the Reserve Bank of India and before onboarding an investor on its platform, the OBPs shall verify the identity of its investors and sellers by requiring them to submit the essential documents and by undertaking all necessary steps for this purpose.

6. Agreement with seller of Debt Securities: The OBPs in order to allow third-party sellers to offer debt securities through their platform, must enter into a written agreement with such entities defining the inter-se relationship, rights, liabilities and obligations before taking up an assignment of offering such securities on its platform.

7.Ensure Transparency – The OBPs shall ensure that all the orders with respect to listed debt securities are routed through the Request for Quote platform (RFQ) of the recognized Stock Exchange and settled through the respective clearing corporations in order to maintain absolute transparency.

8. Issue of receipts: The OBPs shall issue an order receipt to the investor upon placement of an order, a deal sheet to the investor after execution of the order, and a quote receipt to the seller after the execution of the order,

9. Disclosure: The OBPs must identify and disclose all instances of conflict of interest, if any, arising from its transactions or dealings with the related parties on its OBP. Furthermore, the entity must comply with the minimum disclosure requirements for securities offered for sale.

10. Risk Profiling: The OBPs must have in place a questionnaire taking into account multiple factors such as risk appetite, age, investment horizon, etc., in order to determine the preferred level of investment risk that an investor or seller intends to take.

11. Code for Advertisement – The OBPs shall ensure at the time of publishing advertisement through means of print media and digital media, that it shall be true, fair unambiguous and contain accurate information and it shall not misrepresent or mislead the investors.

12. Alerts to sellers and investors: The OBPs must ensure that investors and sellers receive regular updates on the status of their respective transactions through SMS, Emails, etc.

13. Safeguards: The OBPs must establish appropriate safeguards and procedures to handle exigencies like suspension or cessation of trading in debt securities.

These requirements aim to ensure compliance, transparency, and investor protection within the operations of registered stock broker functioning as an OBP.

WILL IT DISRUPT THE PRIVATE PLACEMENT NORMS?As discussed, since the OBPs allows third parties to sell debt securities through their platform, a question may arise that whether the securities offered by companies through private placement can be transacted through these OBPs.

The Companies Act, 2013 defines “private placement” in the following manner:(ii) “private placement” means any offer of securities or invitation to subscribe securities to a select group of persons by a company (other than by way of public offer) through issue of a private placement offer letter and which satisfies the conditions specified in this section.

That it is well established fact that in case of private placement, the initial offer of securities or invitation to subscribe the securities have to be done privately. Thereafter, once the debt securities are issued, they are freely transferable even for companies.

However, as a result of no restrictions on the transfer of debt securities it came to the light of the SEBI at the time of analyzing the data of issuance of listed debt securities on private placement basis subscribed by and further offered for sale by some bond platforms, and it observed that in some instances, the entire issuance was sold to more than 200 investors within 15 days from the date of allotment, which in essence, is in violation of the private placement.

To address this situation, the Committee suggested that a lock-in period of six months may be introduced on selling of these securities. However, the SEBI considering the fact that, inserting the lock-in period, may rob the investors from liquidity and the opportunity to exit their investments, if so desired.

Furthermore, the pool of investors on OBPs may include mutual funds or other institutional investors, in which case if restriction is imposed upon them to liquidate the investments, there can be ramifications which could have large scale implications. Therefore, it was felt prudent to not to include the lock-in provisions. .

AMLEGALS REMARKS

That the introduction of regulatory framework for OBPs in India is a welcome move made by SEBI, as with the bond market offering tremendous scope for development, particularly in the non-institutional space, there was a high need for a regulatory framework to ensure fairness, transparency and security in operations of the OBPs in India.

The mandatory registration of OBPs as stock broker will ensure that such OBPs comply with the KYC norms and the requirements will be applicable while registering clients on bond platforms and the Net worth and deposit requirements prescribed for stock brokers will ensure that the bond platform has a sound and stable financial health.

– Team AMLEGALS, assisted by Ms. Tisha SharmaFor any query or feedback, please feel free to get in touch with tanmay.banthia@amlegals.com or himanshi.patwa@amlegals.com