INTRODUCTION

The Government of India notified the Bilateral Netting of Qualified Financial Contracts Act, 2020 (“Act, 2020”) on 28.09.2020, to provide a regulatory framework to the Qualified Financial Market Participants entered into a Qualified Financial Contract (“QFC”) for setting off counter claims against each other to determine a single net payment obligation due from one counterparty to the another, rather than making multiple gross payments.

The Government of India has introduced the Act, 2020 to ensure financial stability and promote competitiveness in Indian financial markets, as prior to the introduction of the Act, 2020, the transactions which were outside the purview of the Clearing Corporation of India (“CCI’) such as, Over The Counter (“OTC”) Derivatives contract entered between the parties, the parties had to allocate a gross value instead of a single net liability.

Further, the party who had undertaken liability had to keep aside such appropriate capital as security to pay off such liability in the future, as a result of which, a substantial amount of capital used to get trapped and could not be used for any other purposes, which reduced liquidity in the financial market, which in turn slowed down the financial growth of our country.

In this article, we attempt to discuss what is Bilateral Netting, its Applicability, the key aspects of the Act, 2020, and how Bilateral Netting will be advantageous for strengthening the Financial Stability of our country.

WHAT IS BILATERAL NETTING

Bilateral Netting is a mechanism to mitigate financial risk. It is a mechanism wherein parties enter into a legally-binding agreement which enables them to consolidate and/or offset all the claims against each other into one single legal obligation.

This mechanism of consolidating and/or offsetting of claims against each other will help the financial institutions to measure credit exposure on net basis as opposed to gross basis, which will provide security n undertaking a transaction, especially in the event of bankruptcy,

Types

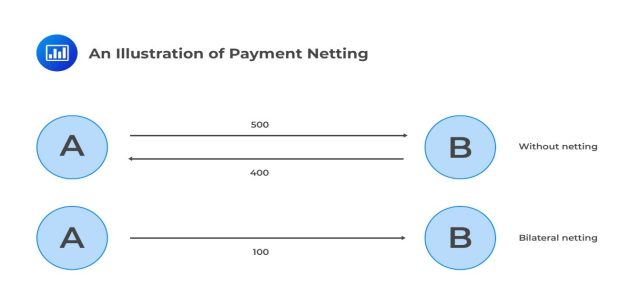

1. Payment Netting/Bilateral Netting

It is a mechanism, in which if counterparties are entering into a multiple cash flows during a day, the counterparties can agree to consolidate and off set claims against each other to determine single payment, which will be paid by the party that owes it. The utilization of Payment Netting reduces Settlement Risk.

2. Close-out Netting –

It works exactly similar to the mechanism of Payment Netting. However, it take place only in cases, when there is an event of a default or the other party has gone into Bankruptcy and is no longer able to make good upon his obligation.

3. Multilateral Netting –

In case there are, more than two parties involved in transaction who has counter claim against each other, which is required to be consolidated and off set, then netting of such transactions will be considered as Multilateral Netting. Multilateral Netting is exercised through a clearinghouse or a central exchange. In India, Multilateral Netting is exercised through a central counterparty, namely the Clearing Corporation of India.

How It Works

How it will help Strengthen the Financial Sector of India

In a case, wherein Bank 1 (“B1”) and Bank 2 (“B2”), both are looking to lend capital and charge interest to gain profits, and B1 is approached by a Company (“C1”) for a loan of Rs. 200 Crore to expand its business. C1 financial records are unimpressive and have a credit rating A. However, C1 is offering an attractive interest rate of 16% as opposed to the usual 12%.

B1 is a Bank that does not lend capital to the company with having a credit rating below AA. However, B1 believes that its expansion plan may work out, whereas B2 believes that the expansion plan of C1 will be successful and is a Bank, which can lend capital to a company having a credit rating of A.

B2 approaches B1 and proposes that in the event C1 defaults on its loan, B2 shall pay the amount in its place. However, until maturity or in case of default, B1 will have to pay a premium of 5% of the loan every year i.e., Rs. 20 Crore each year. This transaction in Banking parlance is known as a “Credit Default Swap” (“CDS”).

Now subsequently, B2 is approached by a Company (“C2”), for a loan of Rs. 300 Crore. C2 financials are poor, and it has a credit rating of BB. However, is offering an attractive interest rate of 16%. This time B2 is unsure about providing loan, whereas B1 thinks that C2 has a great plan and will not default. Therefore, Now, B1 enters into CDS with B2, wherein B2 agrees to pay 5% of the loan every year to B1 i.e., 30 Crore.

B1 and B2 can do this Credit Default Swap CDS arrangement as many times as it likes. However, the authorities would want to ensure that Banks stay in a position to honour the obligations for which it has entered into a CDS arrangement. Therefore, prior to the introduction of Bilateral Netting in India, when Banks had to lend capital on a gross basis, the Banks had to keep aside the equivalent of capital to honour its obligation at the end of the maturity period.

Now, in our case, since there are two streams of cash flow i.e., Rs. 200 Crore from B1 to B2, and Rs. 300 crore vice versa. Rs. 200 Crores will be kept aside by B2 and Rs. 300 Crores by B1. In aggregate, 500 Crores are kept in abeyance, which will stay out of the economy.

However, with the introduction of the Act, 2020, B1 and B2 will now be able to consolidate all the claims against each to determine a single net liability, which would be Rs. 10 Crore to be paid from B2 to B1, which would mean that instead of the Rs. 500 crores that were previously kept in abeyance by both banks, only B1 will have to earmark Rs. 200 Crores, thus freeing up Rs. 300 Crores worth of capital. This can lead to a spur in lending and investment, thereby strengthening the financial sector and our economy.

KEY FEATURES OF THE ACT

1. Qualified Financial Market Participants (“QFMP”)

The Qualified Financial Market Participants in lieu of Section 2(o) of the Act are –

a. Banks and Non-Banking Financial Companies;

b. an Individual, Partnership Firm, Company, or any other person or body corporate incorporated in India or in any other country, including any international or regional development bank or other international or regional organization;

c. Insurance and Re-Insurance Company;

d. Pension Fund regulated by Pension Fund Regulatory and Development Authority; and

e. Financial Institution regulated by International Financial Services Centers Authority Act, 2019

2. Regulated Authorities

The Regulatory Authorities in lieu of the First Schedule of the Act are –

a. Reserve Bank of India (“RBI”);

b. Securities and Exchange Board of India (“SEBI”);

c. Insurance Regulatory and Development Authority of India (“IRDAI”);

d. Pension Fund Regulatory and Development Authority (“PFRDA”);

e. International Financial Services Authority (“IFSC”)

3. Applicability

The Act applies to QFCs entered into bilaterally between ‘Qualified Financial Market Participants’ (QFMP), whether through a netting agreement or otherwise, where at least one of the participants is regulated by any of the Regulatory Authorities mentioned above.

4. Close-Out Netting

As discussed earlier, it works exactly like Payment/Bilateral Netting, wherein the counterparties agree to consolidate and off set claims against each other to determine single payment, which will be paid by the party that owes it. However, it take place only in cases, when there is an event of a default or the other party has gone into Bankruptcy and is no longer able to make good upon his obligation.

In lieu of Section 6 of the Act, 2020 Close-out Netting can be enforced by the non-defaulting party against a defaulting party even if Defaulting Party is subject to any injunction, moratorium, insolvency, resolution, winding up, or court order issued under any law.

5. Interplay with Insolvency Laws

The Act, 2020 have been provided with the power to circumvent several statutes, especially the Insolvency and Bankruptcy Code (“I&B Code”) in order to achieve the desired goal of strengthening the Financial Sector of India.

The I&B Code provides close-out netting only for limited kinds of counterparties, as can be inferred from Section 2 read with Section 36(4)(b) of the I&B Code. However, the introduction of the Act, 2020 has changed the entire scenario by allowing close-out netting for all the Qualified Market Participant who enters into QFC’s.

CHALLENGES

The Government of India introduced the Act, 2020 with the intention of releasing capital kept in abeyance to increase liquidity in the financial market of India. However, there are various challenges being faced that are –

- Struggle with the interpretation, reviewing current agreements, reporting formats, and the inability of systems to adapt to these computation methods.

- In evaluating existing ISDA agreements for netting clauses

- Treatment for netting between GMRA vs ISDA

- Evaluating permissibility for cross-product netting

- Complexity in exposure computation:

- Deciding netting sets across exposure categories

- Changes in replacement cost (“RC”) and potential future exposure (“PFE”)

RECOMMENDATIONS

I. Financial Institutions, especially Banks shall identify the netting sets (i.e., groups of transactions with a single counterparty that are subject to a legally enforceable bilateral netting arrangement).

II. Evaluate the existing agreements with counterparties to check whether the Act, 2020 will be applicable based on the agreement type, their existence, parties involved, and jurisdictions. It the Act, 2020 is not applicable it shall be revisited and renegotiated with the help of the legal team.

III. Convert existing counterparties into netting sets and make it a continuous process, as new agreements are signed (including with its own offshore units or parent entity).

IV. Understand calculation scenarios for netting sets across RC, PFE, Net to Gross Ratio (“NGR”), and exposure computations as well as in the case of reports and reverse-repos.

V. Revise the regulatory/ financial reporting framework to incorporate the impact on data definitions for reporting, aggregation, and segregation logics.

AMLEGALS REMARKS

The Government of India with the introduction of the Act, 2020 had provided an unambitious Bilateral Netting, to increase liquidity and encourage the price efficiency of derivative products by facilitating optimal use of capital thereby enabling banks to increase credit limits for counterparties and clients.

The Government has completed an important milestone by passing this Act. Financial products and derivatives have only become more complex over time. For modern financial markets, it is increasingly important that this agreement extends beyond the contract’s parties and is encoded in the legal framework.

Risk is an inherent feature of every market, but uncertainty in the legal and regulatory framework is a feature that few financial systems can afford if they hope to invite meaningful participation. The expectations for the impact of the Act are high and the next few years will be interesting to watch as regulators take steps to operationalize the Act.

– Team AMLEGALS assisted by Mr. Vinay Sachdev (Intern)

For any queries or feedback, please feel free to get in touch with himanshi.patwa@amlegals.com or tanmay.banthia@amlegals.com.